TaxSaving Investments: ELSS, PPF & More (Overview): No-Spend Challenge (2025)

Tax-Saving Investments: ELSS, PPF & No-Spend Plan (2025)

Table of Contents

🧭 What Counts as “Tax-Saving Investments” in 2025 (and Why It Matters)

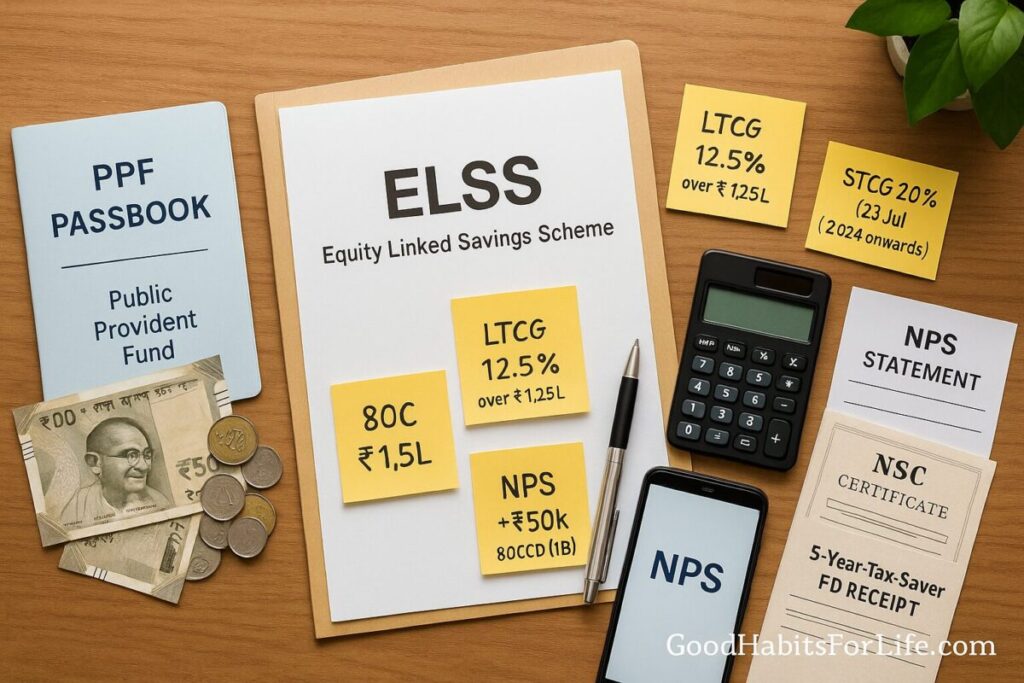

“Tax-saving investments” generally refer to products eligible for deductions mainly under Section 80C (up to ₹1.5 lakh a year in the old tax regime)—for example ELSS mutual funds, PPF, NSC, 5-year tax-saver FDs, SCSS, certain insurance premiums, tuition fees, and home-loan principal; NPS adds a separate ₹50,000 via Section 80CCD(1B). Income Tax DepartmentNational Pension System Trust

Why it matters in 2025: From 23 July 2024, capital-gains rules changed. For listed equity and equity mutual funds (including ELSS), LTCG above ₹1.25 lakh/year is taxed at 12.5% (Section 112A). Short-term equity gains are 20% on/after that date. Plan redemptions and rebalancing with these thresholds in mind. Income Tax India

ELSS in one line: Open-ended equity fund with ≥80% equity, 3-year lock-in, eligible under 80C (old regime). SEBI Investor

PPF in one line: 15-year government-backed account; contribution qualifies under 80C (old regime) and interest/maturity are tax-free (Sec 10)—EEE status. NSI India

NPS in one line: Retirement account with extra ₹50,000 under 80CCD(1B); employer contributions may also be deductible. National Pension System Trust

First decision: Choose your tax regime. The new regime is default and disallows most Chapter VI-A deductions like 80C (with limited exceptions). If you want 80C benefits, opt for the old regime. Income Tax Department+1

✅ Quick Start: Pick Your Tax Regime, Then Your Mix

-

Confirm regime for FY 2025-26/AY 2026-27. If you need 80C, select old regime; otherwise consider the new regime’s lower rates. Income Tax Department

-

Fill your baseline:

-

ELSS (via SIP) if you can accept market risk and a 3-year lock-in. SEBI Investor

-

PPF for guaranteed, tax-free compounding and long-term goals (15-year). NSI India

-

NPS (Tier I) to add ₹50,000 extra deduction via 80CCD(1B). National Pension System Trust

-

-

Top-ups if needed: NSC/5-yr tax-saver FD/SCSS (for seniors) to complete 80C. Income Tax IndiamyScheme

-

Automation: Create standing instructions for SIPs/PPF/NPS the day your salary hits.

-

Compliance dates: For FY 2025-26, investments count up to 31 March 2026; verify LTCG rules when planning exits (12.5% post-23 Jul 2024). Income Tax India

📊 Snapshot Table: ELSS vs PPF vs NPS vs NSC vs 5-Yr FD

| Instrument | Tax benefit | Lock-in/Term | Returns | Tax on returns | Notes |

|---|---|---|---|---|---|

| ELSS | 80C (old regime) | 3 years | Market-linked | Equity LTCG 12.5% over ₹1.25L; STCG 20% (post 23-Jul-2024) | ≥80% equity; SIP allowed. SEBI InvestorIncome Tax India |

| PPF | 80C (old) | 15 years | Govt-set, reviewed quarterly | Tax-free (Sec 10) | EEE status, loan/partial withdrawal rules. NSI India |

| NPS (Tier I) | 80C + 80CCD(1B) extra ₹50k | Till retirement | Market-linked (equity/debt mix) | Partial tax at exit per rules | Employer 80CCD(2) also available. National Pension System Trust |

| NSC | 80C (old) | 5 years | Fixed | Interest taxable (with reinvestment benefit) | Govt small-savings. Income Tax India |

| 5-yr Tax-Saver FD | 80C (old) | 5 years | Fixed | Interest taxable | Bank/post-office options. |

Small-savings rates are reviewed every quarter; for Jul–Sep 2025 the government kept rates unchanged. Always check the latest circular before investing. The Economic TimesThe Times of India

🛠️ 30-Day No-Spend Challenge → Fund Your 80C

A No-Spend Challenge is a short, time-boxed commitment to buy nothing non-essential so you can redirect cash into investments. Pair it with behavioral tactics to make it effective and repeatable.

Your 30-day plan (repeatable each quarter):

-

Define “needs” vs “wants” for 30 days (food staples, medicine, transit = needs).

-

Freeze non-essentials (delivery apps, apparel, gadgets, dining out).

-

Ring-fence savings: open a dedicated “Tax-Save” account; set auto-sweep weekly to ELSS SIP/PPF/NPS. (Commitment device.) Professor Nava Ashraf

-

If-Then rules (implementation intentions): “If I get an impulse to buy, then add it to a 48-hour list.” kops.uni-konstanz.de

-

Default-boost: Increase SIPs by ₹500–₹1,000/month after every salary increment (“Save More Tomorrow” idea). Chicago Journals

-

Weekly review (10 min): Track ₹ saved → invest by Monday morning.

Why it works: Commitment accounts curb present bias; implementation intentions turn intentions into action; auto-escalation exploits inertia in your favor. Professor Nava Ashrafkops.uni-konstanz.deChicago Journals

🧠 Techniques & Frameworks that Make Saving Automatic

-

Implementation Intentions: Write “If X, then Y” rules (e.g., “If it’s the 1st, then invest ₹5,000 into ELSS”). Proven to improve goal attainment. kops.uni-konstanz.de

-

Commitment Devices: Lock funds behind friction (NPS/PPF/ELSS lock-ins or a separate “Tax-Save” account). Evidence shows commitment products raise savings. Professor Nava Ashrafecon.yale.edu

-

Mental Accounting: Label money (e.g., “March-80C”). People treat labeled buckets differently—use it to protect investments. Wiley Online Library

-

Auto-Escalation: Pre-commit to raise SIPs with increments (the SMarT approach). Chicago Journals

🗺️ Audience Variations

-

Students/First-Jobbers: Start with PPF (₹500 min) for safety + a small ELSS SIP for growth; consider NPS only after a stable income. NSI India

-

Professionals: Mix ELSS + PPF; add NPS (₹50k under 80CCD(1B)) if in old regime. Automate raises to SIP hikes. National Pension System Trust

-

Parents (Family goals): Prioritize PPF/NSC for predictability; keep ELSS for long-horizon goals (≥5–7 years). Income Tax India

-

Seniors (60+): If eligible, SCSS + PPF extension (if any) + NSC ladder; ELSS only if risk-tolerant. myScheme

⚠️ Mistakes & Myths to Avoid

-

Myth: “80C works in any regime.” Fact: Most 80C deductions are not allowed in the new regime. Income Tax Department

-

Mistake: Waiting till March—cash-flow crunch and poor fund choices. Fix: Start Q1 with SIPs/standing orders.

-

Myth: “ELSS is tax-free at exit.” Fact: Equity LTCG 12.5% beyond ₹1.25 lakh/year applies (post-23 Jul 2024). Income Tax India

-

Mistake: Using emergency funds for lock-ins. Fix: Keep 3–6 months’ expenses liquid before ELSS/PPF/NSC.

🗣️ Real-Life Scripts & Micro-Plans

-

If-Then Script (shopping): “If I want to buy a non-essential, then I’ll wait 48 hours and move the same amount to my ‘Tax-Save’ account.” kops.uni-konstanz.de

-

Payroll Email Snippet: “Please set a standing instruction: transfer ₹8,000 on the 2nd of every month to a SIP in ELSS-Fund-X and ₹4,000 to PPF.”

-

Raise-Day Autopilot: “Increase all tax-saving SIPs by ₹1,000 starting the next payroll after increment.” (SMarT-style.) Chicago Journals

🧰 Tools & Apps

-

Budget/Tracking: Walnut, Money Manager, ETMoney, Wally.

-

Investing: Your bank/NBFC app; broker apps (for ELSS); NPS via eNPS. (Check NPS Trust page for rules/benefits.) National Pension System Trust

-

Block Temptation: Website blockers, prepaid cards for “fun” spend, “no-spend” shared WhatsApp group.

✅ Key Takeaways

-

Decide new vs old regime first; 80C benefits (ELSS/PPF/NSC/SCSS etc.) need the old regime. Income Tax Department

-

Use a core mix: ELSS (growth), PPF (safety/EEE), NPS (+₹50k under 80CCD(1B)). NSI IndiaSEBI InvestorNational Pension System Trust

-

Know 2025 rules: equity LTCG 12.5% above ₹1.25L; plan redemptions accordingly. Income Tax India

-

Run a 30-day no-spend and automate investments; use If-Then plans, commitment devices, and auto-escalation. kops.uni-konstanz.deProfessor Nava AshrafChicago Journals

❓ FAQs

1) Does 80C (ELSS/PPF/etc.) work in the new tax regime?

Generally no. Under Section 115BAC, the new regime disallows most Chapter VI-A deductions (like 80C) with limited exceptions; opt for the old regime to use 80C. Income Tax Department

2) What’s the ELSS lock-in and taxation now?

Lock-in is 3 years. On/after 23 Jul 2024, equity LTCG 12.5% above ₹1.25 lakh per FY; STCG 20%. SEBI InvestorIncome Tax India

3) Is PPF still tax-free?

Yes. Contribution qualifies under 80C (old regime); interest and maturity are exempt under Section 10. NSI India

4) How does NPS fit with 80C?

NPS gives regular 80C (old regime) plus an extra ₹50,000 under 80CCD(1B)—over and above 80C. National Pension System Trust

5) Are small-savings rates stable in 2025?

Rates are reviewed quarterly; for Jul–Sep 2025 they were unchanged. Always reconfirm current rates before investing. The Economic TimesThe Times of India

6) Can seniors claim 80C with SCSS?

Yes—SCSS deposits qualify for 80C (old regime); interest is taxable. myScheme

7) I’m in the new regime—should I still use ELSS?

You won’t get 80C relief, but you may still invest for long-term equity exposure if it suits your risk profile.

8) What’s the fastest way to start now?

Pick regime → set ELSS SIP + PPF/NPS → run a 30-day no-spend → auto-increase SIPs with your next raise. kops.uni-konstanz.deChicago Journals

📚 References

-

Income Tax Dept. — Tax on Long-Term Capital Gains (as amended by Finance Act, 2025): 12.5% LTCG post-23 Jul 2024; ₹1.25L 112A exemption. (PDF) Income Tax India

-

Income Tax e-Filing Portal — New vs Old Tax Regime FAQs (Chapter VI-A deductions largely not allowed in new regime). Income Tax Department

-

SEBI Investor — ELSS overview (≥80% equity; 3-year lock-in; 80C eligible). SEBI Investor

-

AMFI — SEBI Categorization (ELSS) (3-year lock-in; 80C). AMFI India

-

National Savings Institute (MoF) — Public Provident Fund (80C; Sec 10 tax-free interest/maturity). NSI India

-

NPS Trust (PFRDA) — Benefits of NPS (extra ₹50,000 under 80CCD(1B)). National Pension System Trust

-

DEA/Small Savings — News reports on quarterly rates (Govt left Jul–Sep 2025 rates unchanged; verify current quarter). The Economic TimesThe Times of India

-

Gollwitzer, P.M. (1999) — Implementation Intentions: Strong Effects of Simple Plans, American Psychologist (open-access copies). kops.uni-konstanz.de

-

Ashraf, Karlan, Yin (2006) — Commitment Savings Product in the Philippines, QJE (open-access). Professor Nava Ashraf

-

Thaler & Benartzi (2004) — Save More Tomorrow, Journal of Political Economy (publisher summary). Chicago Journals

Disclaimer: This article is for general education, not financial or tax advice; consult a qualified professional for your specific situation.