TargetDate & Glide Paths: Set It, Check Yearly: AI workflows (2025)

Target-Date Glide Paths: Set & Yearly Check (AI, 2025)

Table of Contents

🧭 What & Why: Target-Date Funds and Glide Paths

What is a target-date fund (TDF)?

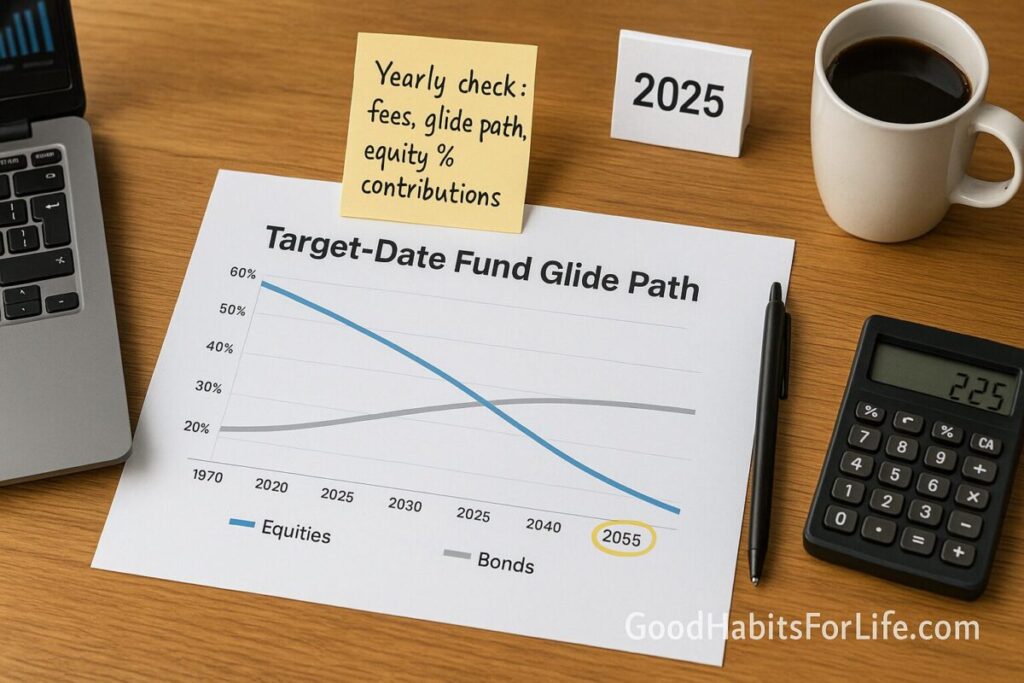

A TDF is a diversified fund that automatically adjusts its stock/bond mix as you approach a specific “target year” (e.g., 2055). The pre-set glide path gradually reduces equity exposure over time; the fund also handles diversification and rebalancing for you. Investor+1

Why it helps:

-

Automatic de-risking as the target year nears—so your portfolio’s risk reduces without manual tinkering. FINRA

-

Behavioral guardrails—one fund, one goal, fewer timing mistakes.

-

Professional portfolio design using broad index core and bond sleeves.

-

Lower-maintenance habit: pair it with a simple annual review checklist.

2025 landscape in brief: Providers are keeping higher equity “early on” and sometimes higher-for-longer equity at the end of the glide path to balance longevity and inflation risks—designs do vary, so read your fund’s specifics. marketing.morningstar.comVanguard

✅ Quick Start: “Set It, Check Yearly” in 20 Minutes

Do this today:

-

Pick your TDF year closest to when you’ll retire (or need the money). Example: retiring in 2055 → “2055” TDF. FINRA

-

Verify the glide path in the fact sheet: equity % now, at retirement, and 10–15 years after. Note if it’s “to” (reaches conservative mix at retirement year) or “through” (continues reducing risk beyond retirement).

-

Check fees (expense ratio) and compare peers using FINRA’s Fund Analyzer or SEC resources. Favor low, transparent costs. FINRAInvestor+1

-

Confirm rebalancing policy and whether the fund holds multiple underlying index funds (typical).

-

Automate contributions via your plan/payroll.

-

Calendar a 1×/year review (month of your birthday) to re-check: fees, glide path fit, and your personal risk/retirement date.

Yearly Review (10-minute checklist):

-

Expense ratio unchanged or still competitive? (screenshot/analyze with FINRA tool) FINRA

-

Asset mix aligns with your time horizon and risk tolerance?

-

“To vs through” still right for your retirement income plan?

-

Any big life changes (retirement date, pension status, risk tolerance) requiring a different TDF year?

🛠️ 30–60–90 Day Habit Plan

Days 1–30: Set & Document

-

Pick TDF + automate contributions.

-

Save fund fact sheet + glide path chart (PDF).

-

Run FINRA Fund Analyzer for your fund vs two peers; paste the results in a one-page note. FINRA

Days 31–60: Stress-Test & Guardrails

-

Calculate cash buffer for the first 6–12 months of retirement expenses (kept in cash/short bonds).

-

Note your withdrawal approach (e.g., guardrails, % withdrawal bands).

-

If within 10 years of retirement, review sequence-of-returns exposure; consider slightly more conservative TDF or adding short-duration bonds/cash for near-term needs. Callan

Days 61–90: Automate the Yearly Check

-

Create a recurring calendar task: “TDF Annual Review.”

-

Build a one-page AI review template (see Workflows) to re-run each year.

-

If your plan allows brokerage window, shortlist lower-cost target-date options for potential switch (if fees/performance warrant).

🧠 Techniques & Frameworks (Risk, “To vs Through,” Rebalancing)

1) Understanding glide path design

-

Starting equity: Many series start high in equities for long horizons; the exact % varies by provider and philosophy. Vanguard

-

End-point equity: Some series keep higher equity into retirement to address longevity/inflation; others de-risk more. Compare the end-of-path equity level across providers. marketing.morningstar.com

-

Personalization: Evidence suggests personalized glide paths (health, wealth, risk tolerance, pension) can improve retirement income sufficiency—TDFs are one size, but your needs may differ. CFA Institute Research and Policy Center

2) “To” vs “Through”

-

“To”: reaches its most conservative mix at the target year; good if you plan to annuitize or hold a bond/cash ladder at retirement.

-

“Through”: keeps adjusting after retirement; good if you’ll stay invested for decades with flexible withdrawals.

3) Sequence-of-returns risk (SoRR)

Losses early in retirement can permanently dent portfolio longevity when you’re withdrawing. Mitigations: cash/bond buffers, flexible withdrawals, and appropriate equity at retirement. Callan

4) Rebalancing

Rebalancing keeps risk on-target. Many TDFs rebalance automatically; if you DIY, annual or bands-based rebalancing are common approaches. Research notes when rebalancing can or cannot boost returns; its primary purpose is risk control. Schwab BrokerageMorningstar

5) Equity level debates

Industry analysis explores whether TDFs should allocate more to equities; weigh growth vs. drawdown risk, especially within 10–15 years of retirement. Morningstar

🤖 AI Workflows (2025): One-Page Annual Review

Goal: A repeatable, 10-minute AI-assisted check that yields a single-page summary you store in your notes.

A) “Know My Fund” Prompt

“Summarize [Fund Name/Ticker] target-date fund: current equity %, end-of-glide equity at retirement and 10 years after, ‘to’ or ‘through,’ expense ratio, rebalancing method, underlying funds, and key risks. Return a table + 3 bullets.”

B) “Compare Peers” Prompt

“Compare [Fund A] vs [Fund B] vs [Fund C] on expense ratio, equity at retirement, ‘to/through,’ bond sleeve type (core vs plus), and historical drawdowns. Give a recommendation matched to a retire-in-[Year] investor who wants [low/moderate/high] risk.”

C) “Fee Check” Prompt (with tool result pasted)

“Using this FINRA Fund Analyzer output, explain the 10-year cost difference vs the median peer and whether a switch is justified. Discuss non-fee tradeoffs (glide path, risk, rebalancing).” FINRA

D) “SoRR Guardrails” Prompt

“I’m [X] years from retirement. Build a 2-bucket plan (cash/short bonds + TDF) to reduce sequence-of-returns risk and specify when to refill the cash bucket.” Callan

E) “One-Page Brief” Prompt

“Create a one-page 2025 TDF review with action items, watchlist (fees, glide path changes), and next review date.”

(Tip: store these prompts in a pinned note; run them each year with updated fact sheets.)

👥 Audience Variations

Students / Early-Career (20s–30s)

-

Choose a TDF roughly 30–40 years out. High equity is normal—stick with it through volatility.

-

Keep fees low; small differences compound over decades. Investor

Parents (mid-career)

-

If retirement is 15–25 years out, confirm end-of-path equity aligns with your comfort during college-spending years.

-

Consolidate stray accounts into plan options with lower fees and solid TDFs.

Professionals (10–15 years out)

-

Audit SoRR: ensure the glide path’s equity at retirement fits your drawdown sensitivity. Consider a separate 1–2 years of expenses in cash/short bonds. Callan

Seniors / Near-Retirees (0–10 years)

-

Verify whether the series is “to” or “through.”

-

Map withdrawals: which account first, tax considerations, and when to tap the cash buffer.

Teens (learning phase)

-

Learn the concept with a mock 2070 fund; understand compounding and why fees matter.

⚠️ Mistakes & Myths to Avoid

-

Myth: “All TDFs are the same.” Reality: fees, glide paths, and end-of-path equity levels vary widely. Compare before choosing. marketing.morningstar.com

-

Mixing a TDF with lots of other funds. You may unintentionally override the glide path and raise risk.

-

Ignoring fees. Even 0.5–1.0% annual differences can materially cut long-run wealth. Use Analyzer tools. Investor

-

No yearly check. Set-and-forget doesn’t mean never review.

-

Wrong target year. Choosing too conservative/aggressive a date skews risk vs need.

-

No cash buffer near retirement. Heightens sequence risk during bear markets. Callan

💬 Real-Life Examples & Scripts

Example 1 — Age 30, retires ~2055

-

Chooses 2055 TDF; expense ratio 0.12%.

-

Yearly AI review confirms equity ~85–90% now; “through” design post-retirement.

-

Action: stay the course; auto-increase contributions +1%/year.

Example 2 — Age 58, retires ~2032

-

In 2030s TDF; checks end-of-path equity (e.g., ~45–55%).

-

Builds 12 months cash; adopts flexible withdrawals (skip raises during down years).

-

Script to HR:

“Please confirm whether our default TDF is ‘to’ or ‘through’ and share the latest glide path and expense ratio fact sheet.”

Example 3 — Switching due to fees

-

Uses FINRA Fund Analyzer: current fund projected 10-year cost ₹X more than peer; AI brief recommends switching if glide paths are comparable. FINRA

🧰 Tools, Apps & Resources (quick pros/cons)

-

FINRA Fund Analyzer — clear fee comparisons; needs manual ticker input. FINRA

-

SEC Investor.gov — plain-English explainers on TDFs and fees; not product-specific. Investor+1

-

Provider Fact Sheets (e.g., Vanguard, Fidelity) — definitive glide path charts; provider-specific. Vanguardinstitutional.fidelity.com

-

Morningstar Landscape (2025) — broad industry view of equity levels and trends; detailed PDF. marketing.morningstar.com

-

Callan Notes on SoRR — practical framing of sequence risk in TDFs. Callan

📌 Key Takeaways

-

Set a target-date fund matched to your retirement year; it delivers a professional glide path and rebalancing. Investor

-

Once a year, check fees, glide path fit, and your time horizon; low-cost and right-risk beat constant tinkering. Investor

-

Near retirement, address sequence-of-returns risk with buffers and flexible withdrawals. Callan

-

Use AI workflows to create a one-page review and keep decisions simple, repeatable, and documented.

❓FAQs

1) How do I choose the right target year?

Pick the fund closest to your planned retirement year; adjust if you’re meaningfully more/less risk-tolerant than average. FINRA

2) What’s the difference between “to” and “through”?

“To” reaches its conservative mix at the target date; “through” continues de-risking after. Choose based on whether you’ll keep investing during retirement.

3) Do I need to rebalance if I use a TDF?

No—the fund does this internally. If you add other funds, you may upset the intended allocation. Investor

4) Are all TDFs low-cost?

No. Fees vary a lot. Compare expense ratios; small differences compound over time. Investor

5) Should I hold cash/bonds separately near retirement?

Many do, to reduce sequence risk and fund withdrawals in down markets. Callan

6) Can I switch TDF providers later?

Yes—evaluate taxes (if in taxable accounts), fees, and glide-path differences. Use FINRA/SEC tools for fee comparisons. FINRA

7) What if my 401(k) doesn’t offer TDFs?

Replicate the idea with a broad stock index + bond fund and annual rebalancing. Schwab Brokerage

8) Is a higher end-of-path equity better?

Not always—it can improve longevity protection but raise drawdown risk. Compare designs and your comfort level. marketing.morningstar.comMorningstar

9) How often should I review?

Annually, or after major life changes. That’s enough for most investors. FINRA

10) Do TDFs guarantee returns?

No. They manage allocation and rebalancing but cannot eliminate market risk. Investor

📚 References

-

SEC Investor.gov — Target Date Funds (overview). Investor

-

FINRA — Save the Date: Target-Date Funds Explained. FINRA

-

Morningstar — Target-Date Fund Landscape 2025 (PDF). marketing.morningstar.com

-

Vanguard Institutional — TDF Glide-Path Essentials: Starting Point (2025). Vanguard

-

CFA Institute FAJ — Retirement Income Sufficiency through Personalised Glidepaths (2021). CFA Institute Research and Policy Center

-

Callan — Sequence-of-Returns Risk in TDF Glidepaths (2024). Callan

-

Morningstar — When Rebalancing Creates Higher Returns—and When It Doesn’t (2024). Morningstar

-

Charles Schwab — Rebalancing in Action (2025). Schwab Brokerage

-

SEC Investor.gov — Mutual Fund and ETF Fees and Expenses (2025). Investor

-

FINRA — Using the FINRA Fund Analyzer (tool & methodology). FINRA+1

⚖️ Disclaimer

This article is for educational purposes and is not financial advice; consider speaking with a licensed adviser for your situation.