PPF vs EPF vs VPF: What Fits Your Mix?: AI workflows (2025)

PPF vs EPF vs VPF (2025): What Fits Your Mix?

Table of Contents

🧭 What & Why (clear definitions + benefits)

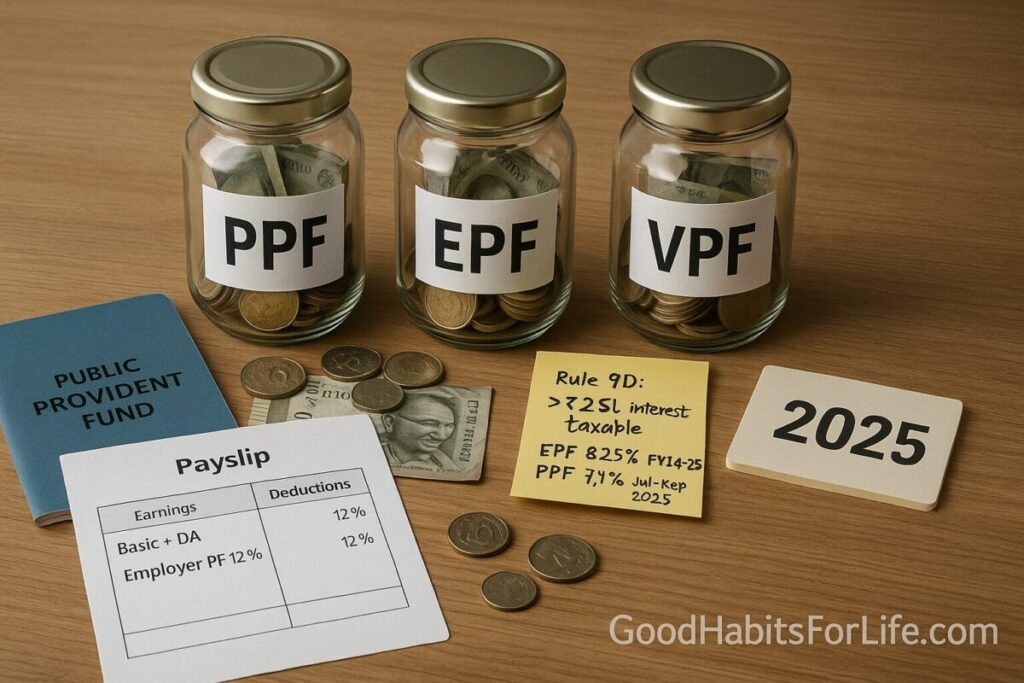

PPF (Public Provident Fund). A 15-year, government-backed account anyone can open; interest is set quarterly (7.1% for Jul–Sep 2025). Contributions and returns enjoy EEE tax (deduction under 80C in the old tax regime; tax-free growth; tax-free maturity). Best for safety and long-term compounding. Department of Economic AffairsNews on AirNSI India

EPF (Employees’ Provident Fund). A mandatory retirement scheme for salaried employees; both employee and employer contribute (generally 12% of basic+DA; establishment-specific rules apply). Interest for FY 2024-25 is 8.25%, credited annually. Great for disciplined, payroll-linked saving. EPF India+1

VPF (Voluntary PF). Your optional extra contribution into EPF above the statutory 12%, earning the same EPF rate and following the same rules. Subject to Rule 9D taxation if your annual employee contributions are high (details below). EPF India

Tax note (Rule 9D). Interest on the employee’s EPF/VPF contributions above ₹2.5 lakh/year is taxable; where there’s no employer contribution, the threshold is ₹5 lakh. Separate “taxable” and “non-taxable” contribution accounts must be maintained for computation. Income Tax India+1

✅ Quick Start: choose your mix in 7 steps

-

Confirm your regime. If you use the old tax regime, you can claim 80C (PPF/EPF/VPF) up to ₹1.5 lakh. In the new regime, 80C doesn’t apply (with limited exceptions outside this scope). Income Tax Department

-

Lock-in tolerance. If you need predictable access within 5–7 years, lean more on EPF/VPF (partial withdrawals/loans under allowed conditions) and less on PPF (15-year lock-in with limited partial withdrawals). EPF IndiaNSI India

-

Tax threshold check (Rule 9D). Estimate your employee EPF+VPF across the year. If it may exceed ₹2.5 lakh, consider shifting some surplus to PPF (EEE) to avoid taxable EPF interest. Income Tax India

-

Employer benefits. If your employer contributes to EPF and you’re comfortable with payroll lock-in, add VPF for convenience and higher forced savings. EPF India

-

Safety vs return. EPF historically offers a higher declared rate than PPF this year (8.25% vs 7.1%); both are low-risk. Balance with your tax and liquidity needs. EPF IndiaDepartment of Economic Affairs

-

Execution friction. If HR can raise VPF quickly and you want one-tap saving, tilt to VPF. If you prefer a separate, personal account, tilt to PPF at bank/post office. NSI India

-

Set your split. A common starting point: EPF (mandatory) + VPF (to your Rule 9D limit) + PPF (to fill 80C or EEE need); revisit quarterly when PPF rates reset.

🛠️ 30-60-90 Habit Plan (with checkpoints)

Days 1–30 (Setup & Baseline)

-

Check passbook & projections: Log in to EPFO Member e-Sewa; note YTD employee contributions. Forecast to Mar 31 to see if you’ll cross ₹2.5 lakh. EPF India

-

HR action: File a VPF request (if needed) to reach your target savings without breaching the Rule 9D threshold. EPF India

-

Open/verify PPF: If you don’t have one, open PPF (bank/post office). Plan monthly ECS so you don’t miss the compounding window. NSI India

-

Checkpoint: Contribution plan created; standing instructions set.

Days 31–60 (Optimize & Automate)

-

Date discipline: Prefer 1st–5th of month for PPF deposits to maximize monthly interest calculation convention.

-

Emergency buffer: Keep separate liquidity (3–6 months expenses) so you don’t raid EPF/PPF.

-

Checkpoint: YTD summary reviewed; adjust VPF % if salary changes.

Days 61–90 (Review & Lock routine)

-

Quarterly rates: On/around last working day of the quarter, check MoF update on small savings. Adjust PPF plan if rates change. Department of Economic Affairs

-

Year-end alignment: From Jan–Mar, recheck Rule 9D exposure and tweak VPF to avoid taxable interest if that’s your goal. Income Tax India

-

Checkpoint: Final quarter glide path set; no surprises at year-end.

🧠 Techniques & Frameworks

1) The 3-Lens Fit (Tax–Liquidity–Return).

-

Tax: Old regime 80C favors both PPF and EPF/VPF up to ₹1.5 lakh; beyond that, PPF remains EEE while EPF/VPF can trigger Rule 9D. Income Tax DepartmentIncome Tax India

-

Liquidity: PPF = tight lock-in with limited partial withdrawals; EPF/VPF = partial withdrawals/loans allowed under service/defined conditions. NSI IndiaEPF India

-

Return: FY25 EPF 8.25% vs PPF 7.1% (Q2 FY26). If safety is equal enough for you, rate tilts can guide the marginal rupee. EPF IndiaDepartment of Economic Affairs

2) Rule 9D Guardrail.

Create two mental buckets: “non-taxable” EPF interest (up to ₹2.5 lakh employee contribution, or ₹5 lakh with no employer contribution) vs “taxable” EPF interest (excess). Keep your employee EPF+VPF under the threshold if your aim is tax-free accrual. Income Tax India+1

3) AI Workflows (2025) to pick your mix quickly.

-

PF-Mix Prompt (for ChatGPT/your AI tool):

“Given my monthly basic+DA ₹, employer EPF % , current EPF balance ₹, PPF balance ₹, tax regime (old/new): , target annual retirement saving ₹, suggest an EPF-VPF-PPF split that (a) avoids Rule 9D tax if possible, (b) fills 80C efficiently, (c) keeps ₹__ liquid. Return a monthly plan and year-end projections.” -

Rule 9D Checker: Ask your AI to compute projected FY employee EPF+VPF and flag the first month your cumulative crosses ₹2.5L/₹5L. Income Tax India

-

Quarterly Rate Watch: Have AI set a calendar reminder to check MoF small-savings rates each quarter-end and propose any PPF top-up changes. Department of Economic Affairs

📊 Side-by-Side Comparison (2025)

| Feature | PPF | EPF | VPF |

|---|---|---|---|

| Who can invest | Any resident individual | Salaried employees in covered establishments | Same salaried employee (voluntary top-up) |

| Current interest (ref) | 7.1% (Jul–Sep 2025; quarterly-set) | 8.25% (FY 2024-25; annual credit) | Same as EPF |

| Tax on contribution | 80C (old regime) | 80C (old regime) | 80C (old regime) |

| Tax on interest | Tax-free | Tax-free up to Rule 9D thresholds | Tax-free up to Rule 9D thresholds |

| Lock-in | 15 years (extensions in 5-year blocks) | Till retirement/job change; rules for withdrawals/loans | Same as EPF |

| Liquidity | Limited partial withdrawals/loan | Loans/partial withdrawals per scheme provisions | Same as EPF |

| Employer contribution | None | Yes (split between EPF/EPS) | No |

| Typical use | Safe long-term EEE corpus | Payroll-linked retirement saving | Boost retirement saving via payroll |

Refs: Department of Economic AffairsNSI IndiaEPF India+1Income Tax India

🎯 Audience Variations

-

Students/early-career: Start PPF with small ECS (₹500–₹1,000/month) to lock decades of compounding; rely on EPF once salaried. NSI India

-

Parents (single income): Use EPF/VPF to automate saving; allocate PPF to the non-earning spouse to widen 80C usage under old regime. Income Tax Department

-

Professionals (high income): Max EPF/VPF until you approach Rule 9D; funnel the rest into PPF for EEE (and other instruments as per plan). Income Tax India

-

Seniors (no new EPF): PPF extensions in 5-year blocks can suit low-risk income plans alongside senior schemes (outside scope here). NSI India

⚠️ Mistakes & Myths to Avoid

-

“VPF is a different scheme.” Myth—VPF is just your extra EPF contribution, same interest, same rules. EPF India

-

Ignoring Rule 9D. Large employee EPF/VPF can create taxable interest—plan your split early. Income Tax India

-

PPF last-minute lump sums. Monthly discipline (earlier in the month) typically helps maximize compounding across the year.

-

Assuming 80C under the new regime. Deductions like 80C generally don’t apply there. Income Tax Department

🗣️ Real-Life Examples & Scripts

Example A: Mid-career, old regime

-

Salary basic+DA ₹80,000/month; employer EPF 12%. Target: ₹3.6 lakh/yr retirement saving.

-

Plan: Mandatory EPF ~₹1.15L (employee), VPF ~₹1.35L (to keep total employee EPF+VPF ≤ ₹2.5L under Rule 9D), PPF ₹1.1L to fill 80C & EEE. Income Tax India

Example B: High-income, new regime

-

Doesn’t use 80C.

-

Plan: Mandatory EPF continues; limit VPF to avoid Rule 9D interest tax, send surplus to PPF only if EEE + lock-in match goals (or to other instruments outside this piece). Income Tax India

Email to HR (raise VPF):

Subject: Request to start/modify VPF contribution

Dear HR,

I’d like to start/adjust my VPF to __% of basic + DA from the next payroll cycle. Please confirm the effective month and any form I must sign.

Thanks,

__

Bank instruction (PPF ECS):

Please set a monthly ECS of ₹__ to my PPF A/c no. __ on the 3rd of each month, starting //2025.

🧰 Tools, Apps & Resources

-

EPFO Member e-Sewa / Passbook: Track annual interest credit and YTD employee contributions. EPF India

-

MoF/DEA small-savings notices: Check PPF rate each quarter before top-ups. Department of Economic Affairs

-

PPF Scheme, 2019 (official rules): Eligibility, withdrawals, loans, extensions. NSI India

AI Workflow Prompts (copy-paste):

-

“Compare my EPF-VPF-PPF options given: basic+DA ₹__, employer EPF __%, current balances /, tax regime __. Keep employee EPF+VPF ≤ ₹2.5L unless I confirm otherwise; propose a monthly split and year-end outcome.” Income Tax India

-

“Project whether my EPF interest credit at 8.25% and PPF at 7.1% meets my target ₹__/yr; show sensitivity if rates change ±0.5% next year.” EPF IndiaDepartment of Economic Affairs

📌 Key Takeaways

-

PPF = EEE, long lock-in, 7.1% (Q2 FY26). Department of Economic Affairs

-

EPF = payroll-linked, 8.25% (FY25), partial access rules. VPF is the voluntary add-on to EPF. EPF India

-

Rule 9D can make interest on high employee EPF/VPF taxable—plan your limits. Income Tax India

-

Use the 30-60-90 plan and AI workflows to set, automate, and periodically optimize your mix.

❓ FAQs

1) Is VPF better than PPF for 2025?

If you need higher declared rates and easy payroll deduction, VPF (same rate as EPF, 8.25% for FY25) can edge PPF (7.1% this quarter). If you value EEE certainty without Rule 9D exposure, PPF may fit better. EPF IndiaDepartment of Economic Affairs

2) Can I invest in all three—PPF, EPF, and VPF—together?

Yes. Many do: EPF mandatory, VPF to a target level, PPF to complete 80C/EEE goals. Just watch the Rule 9D limit on employee EPF+VPF. Income Tax India

3) Do I get 80C on EPF/VPF/PPF in the new tax regime?

Generally no (80C applies to the old regime). Decide regime first; then optimize contributions accordingly. Income Tax Department

4) What if I change jobs—does EPF continue?

You can transfer EPF; service continuity matters for withdrawal rules (e.g., 5-year horizon). EPF India

5) Is EPF interest taxed when it’s credited late?

Taxability follows Rule 9D thresholds and how EPF interest is reported; monitor the year of credit in your passbook/AIS if timing shifts. Income Tax India

6) How much VPF can I contribute?

You can contribute above the statutory 12% employee rate (subject to scheme provisions and payroll setup). Check with HR; some establishments allow higher-wage contributions per para 26(6). EPF India

7) Can I take loans from PPF or exit early?

PPF allows loans and limited partial withdrawals under specific rules; full closure is restricted. NSI India

8) Why is EPF rate different from PPF rate?

EPF is declared annually by EPFO (subject to government approval), while PPF is a small-savings scheme with a quarterly rate set by MoF. EPF IndiaDepartment of Economic Affairs

📚 References

-

Department of Economic Affairs, Small Savings Rates for Q2 FY 2025-26 (Jun 30, 2025). Department of Economic Affairs

-

All India Radio, Rates unchanged for Q2 FY26 (Jun 30, 2025). News on Air

-

EPFO Circular, Declaration of EPF ROI 2024-25: 8.25% (May 26, 2025). EPF India

-

EPFO, CBT press note recommending 8.25% (Feb 28, 2025). EPF India

-

CBDT, Notification No. 95/2021 – Rule 9D (Aug 31, 2021). Income Tax India

-

CBDT, Circular No. 24/2022 – Clarification on Rule 9D thresholds (Dec 7, 2022). Income Tax India

-

National Savings Institute, PPF Scheme, 2019 (official rules). NSI India

-

EPFO FAQ, Voluntary contributions & withdrawals/transfer. EPF India

-

EPF Scheme, Contribution & provisions (official). EPF India

Disclaimer: This article is educational financial information, not investment or tax advice; please consult a qualified advisor for your situation.