Financial Stress Toolkit: Breathe Budget Boundaries: No-Spend Challenge (2025)

Financial Stress Toolkit: Breathe, Budget & No-Spend (2025)

Table of Contents

🧭 What Is Financial Stress—and Why It Spikes Spending

Financial stress is the anxious, overwhelmed state that arises when money demands feel bigger than your resources. Surveys consistently show money and the economy are top stressors for adults; in 2024, the APA reported the economy as a significant stress source for most Americans. Financial concerns remain widespread globally, with cost-of-living pressures persisting across OECD countries. Chronic money stress can also reinforce a loop with mental health and debt—each making the other worse.

Why this toolkit works: Stress narrows attention and pushes us into short-term choices (present bias). A calm nervous system + clear, simple rules reduces impulsive purchases and keeps you moving toward savings and debt goals.

Core outcomes you’re aiming for

-

A calmer baseline (so choices improve)

-

A budget you can use without thinking

-

Guardrails (“boundaries”) that prevent leaks

-

A quick emergency buffer (even ₹5,000–₹10,000 / $100–$200)

-

A repeatable weekly rhythm you can sustain

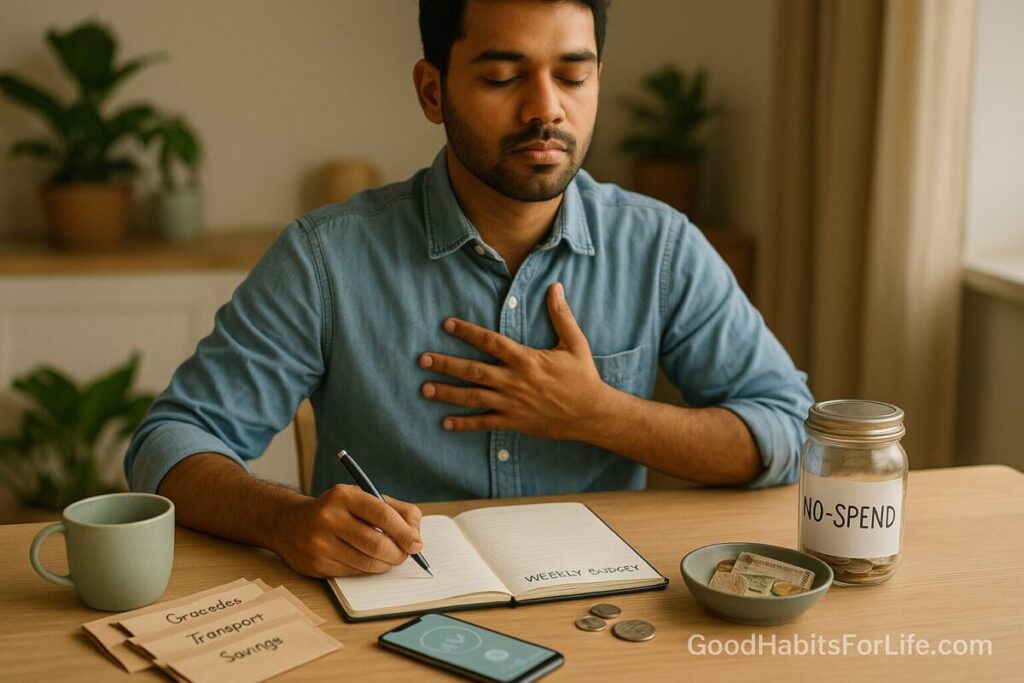

✅ Quick Start: Today’s 30-Minute Reset

Timeboxed, do-this-now routine

-

Breathe (5 min). Sit, one hand on belly. Inhale through nose 4s, belly expands; exhale through pursed lips 6s. Repeat 10–20 cycles.

-

Money snapshot (10 min). Jot three numbers:

-

Income (monthly net)

-

Fixed costs (rent, utilities, loans, basic groceries, transport)

-

Weekly spend cap = (Income – Fixed costs – Minimum savings) ÷ 4

-

-

Budget boundaries (5 min). Pick 3 rules (see list below).

-

No-Spend prep (5 min). Define “essentials only” for 14 days. Start tomorrow.

-

Automate one thing (5 min). Schedule a small transfer on payday to an Emergency Fund sub-account.

One-page budget template (copy this to Notes):

-

Income (monthly): ______

-

Fixed costs (total): ______

-

Minimum savings autopay: ______ (e.g., ₹2,000 / $25)

-

Weekly spend cap: ______ (card/cash for groceries + variable spend)

-

Sinking funds (optional): utilities top-ups, annual fees, gifts, travel

🧠 30-60-90 Day Roadmap

Day 0–30: Stabilize

-

Daily 2–5 minutes of belly breathing (habit trigger: after brushing teeth).

-

Run 14-day No-Spend (details below).

-

Build ₹5,000–₹10,000 / $100–$200 mini-emergency fund.

-

Track weekly spend once/week; fix leaks (subscriptions, fees).

-

One bill negotiation (internet, mobile, or card fee).

Day 31–60: Strengthen

-

Increase emergency fund toward ₹25,000–₹40,000 / $400–$600.

-

Add 2–3 sinking funds (medical, school, vehicle).

-

Create “friction” for impulse buys (24-hour rule, uninstall 1 shopping app).

-

Implement pay-raise rule: auto-increase savings % with any income bump.

Day 61–90: Grow resilience

-

Emergency fund to 1 month of basic expenses (target).

-

Pre-commit savings (standing orders) and recurring debt overpayments.

-

Quarterly “values audit”—align spending with top 3 life priorities.

-

Review boundaries; keep only the 3 that move the needle.

🛠️ Techniques & Frameworks That Actually Work

Breathing to think clearly

-

Diaphragmatic breathing and paced breathing reduce physiological arousal and anxiety, supporting better decisions. Start with 4-in/6-out for 2–5 minutes.

Behavioral finance tactics

-

Pre-commitment (Save-More-Tomorrow style). Decide now to raise savings with each pay increase.

-

Implementation intentions. “If I feel urge to buy, then I add it to Wish-Later and revisit in 24 hours.”

-

Friction. Remove saved cards from browsers; delete shopping apps; require OTP for purchases.

-

Temptation bundling. Only check favorite shop sites while walking on treadmill or after finishing weekly review.

Habit science

-

Habits form by repetition in a stable context; many money routines “click” within weeks, though timelines vary. Anchor breathing and budget check-ins to existing routines.

⚠️ Budget Boundaries: Rules That Protect You

Pick 3–5 to start; revisit monthly.

-

24-Hour Pause Rule: Non-essential buys wait 24 hours.

-

One-Cart Rule: Weekly grocery shop with a list; no mid-week top-ups.

-

Cash Envelope for Discretionary: Load a set weekly amount; when it’s gone, it’s gone.

-

Single-Subscription Rule: One entertainment service at a time.

-

Two-Tap Unsubscribe: Audit & cancel unused subscriptions monthly.

-

Social Spend Cap: Fixed monthly cap for eating out, events.

-

Returns Ritual: Calendar holds for return windows; batch returns every Saturday.

-

BNPL Ban (or strict cap): Use only for essentials and only if repaid within the cooling-off period.

Allowed vs Paused (example for No-Spend)

| Category | Allowed | Paused |

|---|---|---|

| Groceries | Base staples, fresh produce | Premium snacks, gourmet items |

| Transport | Commuting, fuel, necessary repairs | Rideshares for convenience |

| Health | Prescriptions, essential care | Wellness add-ons, supplements (non-essential) |

| Home | Utilities, basic supplies | Décor, upgrades |

| Personal | Hygiene basics | Clothing, gadgets, cosmetics |

| Fun | Free/low-cost activities | Paid entertainment, takeout (unless pre-planned) |

🧊 No-Spend Challenge (14 Days)

Purpose: Create a short, winnable sprint that resets habits and reveals “mindless” expenses.

Setup (10 minutes)

-

Define essentials (use table above).

-

Pick two free treats (e.g., picnic, park workout).

-

Start a Wish-Later note for anything tempting—review it on Day 15.

Daily cadence

-

Morning: 2 minutes of belly breathing; scan calendar for spending traps.

-

Evening (5 min): Log any spending; celebrate a small win.

-

Trigger plan: “If I want to buy ___, then I add it to Wish-Later and walk for 5 minutes.”

Finish line (Day 15)

-

Tally savings.

-

From Wish-Later, pick one purchase that still feels right and fits the budget.

-

Keep the best two boundaries you discovered.

📚 Audience Variations

-

Students/Teens: Use prepaid card or UPI wallet with a weekly cap; do 7-day No-Spend sprints; prioritize a micro-fund for exams/transport.

-

Parents: Create a family “needs vs wants” list; batch cook to protect grocery budget; kids help with returns.

-

Professionals: Automate savings on payday; set a workday lunch rule (packed lunch 3 days/week).

-

Seniors: Simplify to 1–2 bank accounts; audit recurring charges quarterly; plan low-cost social routines.

-

General/Households: Run couples’ “10-minute check-in” on Sundays—budget, calendars, one improvement for next week.

🧯 Mistakes & Myths to Avoid

-

Myth: “No-spend means no joy.”

Truth: It’s a reset; add free treats and plan celebratory spending after. -

Mistake: Using detailed budgets you never open.

Fix: Keep a one-page view + weekly spend cap. -

Myth: “I’ll save when I earn more.”

Truth: Savings behavior is built at any income; pre-commit small automations now. -

Mistake: Hiding from bills and balances.

Fix: Weekly 15-minute Money Date; face the numbers. -

Myth: “Breathing is woo.”

Truth: Evidence supports paced/diaphragmatic breathing for stress reduction and clearer thinking.

🗣️ Real-Life Examples & Scripts

1) Internet/mobile bill negotiation (phone)

“Hi, I’ve been a customer for X years. My current plan costs ₹__/$ . I’m seeing competitive offers at ₹/$ ____. I’d like to stay—what loyalty discount or lower-tier plan can you move me to today?”

2) Credit card annual fee waiver (chat/email)

“I value the card but the annual fee is hard to justify now. Can you waive or credit the fee, or move me to a no-fee product without affecting my history?”

3) Debt hardship request

“I’m experiencing temporary financial stress. Can we set up a payment plan with reduced interest for the next 6 months? I want to keep paying and avoid delinquency.”

4) Social boundary (text to friends)

“I’m on a 14-day reset—skipping paid outings. Up for a park walk or game night at mine?”

5) Self-talk pattern

“Not now, maybe later.” (Add to Wish-Later; re-check on Day 15.)

🧰 Tools, Apps & Resources (quick pros/cons)

-

CFPB Financial Well-Being tool (quiz): Measures your money well-being; great starting baseline. Pro: evidence-based; Con: U.S.-centric.

-

Budget planners (MoneyHelper, spreadsheets): Free planners to map income/outgoings. Pro: Simple; Con: Manual entry.

-

Envelope/”weekly cap” methods (apps or cash): Puts a hard limit on discretionary spend. Pro: Clear constraint; Con: Needs discipline to maintain.

-

Subscription trackers: Spot and cancel unused services. Pro: Quick wins; Con: May require bank connection.

-

Bank “Spaces/Pots”: Create sub-accounts for goals and bills. Pro: Visual progress; Con: Feature availability varies by bank.

-

Breathing guides (medical org pages): Step-by-step belly/pursed-lip breathing. Pro: Clinically reviewed; Con: Practice required.

🧾 Key Takeaways

-

Calm body first; decisions follow.

-

Keep the budget minimal: income, fixed costs, and a weekly cap.

-

Boundaries beat willpower.

-

Short no-spend sprints reset habits and surface leaks.

-

Automate savings and pre-commit increases.

-

Review weekly; change one thing at a time.

❓ FAQs

1) Is a no-spend challenge safe if I have debt?

Yes—define essentials and keep paying minimums. Use the savings to build a tiny buffer or make targeted extra payments.

2) How long should I no-spend?

Start with 14 days. Repeat if helpful, but avoid “all-or-nothing” for months—sustainability matters.

3) What if an emergency hits during no-spend?

Emergencies are allowed. The challenge is about discretionary spending.

4) What’s the smallest emergency fund worth building?

Even ₹5,000–₹10,000 ($100–$200) helps—research shows many adults struggle with even modest unexpected expenses; small buffers matter.

5) I panic when I open my banking app. Tips?

Do 2 minutes of breathing first. Open balances during a scheduled weekly money date, not randomly.

6) Should I close credit cards to control spending?

Not usually. Consider freezing cards, lowering limits, or product-changing to no-fee rather than closing (which can affect credit history).

7) Are breathing techniques really evidence-based?

Yes—diaphragmatic and paced breathing have documented benefits for stress reduction and can support better decision-making.

8) What if my partner isn’t on board?

Run your own 14-day sprint and demonstrate wins. Invite them to a 10-minute weekly check-in—start with shared essentials, not blame.

9) How do I keep progress after 90 days?

Maintain your top 3 boundaries, keep automation on, and schedule quarterly reviews.

10) I live outside the U.S.—do these resources still help?

Yes—the techniques are universal. For local debt relief or budgeting tools, search your country’s government finance or consumer protection site.

📚 References

-

American Psychological Association. Stress in America 2024 (economy as a significant stressor). https://www.apa.org/pubs/reports/stress-in-america/2024/2024-stress-in-america-full-report.pdf

-

OECD. How’s Life? 2024 (cost-of-living pressures, financial concerns). https://www.oecd.org/en/publications/2024/11/how-s-life-2024_bdcf2f9f.html and In-Brief PDF https://www.oecd.org/content/dam/oecd/en/publications/reports/2024/11/in-brief-how-s-life-2024_5124fb86/eedbe25b-en.pdf

-

Federal Reserve Board. Report on the Economic Well-Being of U.S. Households (2024) (ability to cover a $400 expense). https://www.federalreserve.gov/publications/files/2024-report-economic-well-being-us-households-202505.pdf and data viz https://www.federalreserve.gov/consumerscommunities/sheddataviz/unexpectedexpenses-table.html

-

CFPB. Financial Well-Being Measurement Tool (evidence-based assessment). https://www.consumerfinance.gov/consumer-tools/financial-well-being/

-

Cleveland Clinic. Diaphragmatic breathing & breathwork guides. https://my.clevelandclinic.org/health/articles/9445-diaphragmatic-breathing and https://health.clevelandclinic.org/breathwork

-

CDC/NIOSH (archived). Relaxation techniques (breathing, PMR, meditation). https://archive.cdc.gov/www_cdc_gov/niosh/emres/longhourstraining/relax.html and CDC stacks on paced breathing: https://stacks.cdc.gov/view/cdc/113371/cdc_113371_DS1.pdf

-

Lally, P. et al. (2010). How are habits formed? Eur J Soc Psychol. https://onlinelibrary.wiley.com/doi/abs/10.1002/ejsp.674

-

Thaler, R. & Benartzi, S. (2004). Save More Tomorrow™ (pre-commitment to increase savings). https://www.journals.uchicago.edu/doi/abs/10.1086/380085

-

Ten Have, M. et al. (2021). Debts and common mental disorders: bidirectional links. Soc Psychiatry Psychiatr Epidemiol. (PMC). https://pmc.ncbi.nlm.nih.gov/articles/PMC8043431/

-

UK Government. Debt Respite Scheme “Breathing Space” guidance (legal protections). https://www.gov.uk/options-for-dealing-with-your-debts/breathing-space and creditor guidance https://www.gov.uk/government/publications/debt-respite-scheme-breathing-space-guidance/debt-respite-scheme-breathing-space-guidance-for-creditors

-

MoneyHelper (UK). Budget Planner & tools. https://www.moneyhelper.org.uk/en/everyday-money/budgeting/budget-planner and https://www.moneyhelper.org.uk/en/tools-and-calculators

⚖️ Disclaimer

This article is for education only and is not financial, medical, or legal advice; consider speaking with a qualified professional for your situation.